Government Saving Vodafone-Idea?

Our aim through TVS Weekly is to break down financial stories and concepts simply, explaining what happened and why it matters to you.

No Jargon, no drama! Just stuff that actually makes sense.

Curious? Get more from us on our Instagram, WhatsApp, LinkedIn or YouTube. Our 800K+ family awaits you!

In this week’s newsletter, we’ll learn:

Why is the Government now the biggest shareholder in Vodafone Idea?

How to know if markets are overvalued: Tobin’s Q.

Market Kya Keh Raha Hai Sir?

Vodafone Idea (Vi), India’s third-largest telecom operator, just got a major breather. The Government of India will convert ₹36,950 Cr of Vi’s debt into equity, making it the largest shareholder with a 49% stake.

Investors cheered the move, pushing the share price up 20%. Big-name analysts from Citi, CLSA, and Nomura even slapped on a buy rating. But is this a turning point for Vi, or just another delay before the inevitable end?

Let’s break it down.

How did Vi get here?

Vi’s total dues owed to the government were over 2.2 Lakh Crores with a yearly instalment of around ₹40,000 Cr.

Supreme Court Directive:

In 2020, the Supreme Court ordered telecom companies to pay 10% of their total dues. Since these dues were massive, in 2021, the court granted a 4‑year moratorium for the remaining 90%, deferring its full payment until 2031.

A moratorium is a specific period during which no payments need to be made towards reducing debt. It is allowed during financial hardship.

All wasn’t perfect, as interest was still charged during these 4 years.

With a free cash flow of around ₹15,000 Cr, Vi couldn’t pay the 10% asked. It couldn’t afford the interest accrued during the moratorium either.

Therefore, in 2023, it agreed to convert ₹16,000 Cr of accrued interest into a 33% equity stake.

Fast forward to 2025

The end of the moratorium was still looming. Even after raising ₹20,000+ Cr from private investors, it would not be able to meet the annual payments. Therefore, it converted ₹36,950 Cr of its AGR debt into equity, raising the government’s stake to 49%.

Adjusted Gross Revenue (AGR) is the amount of a telecom operator’s revenue that must be paid to the government as fees for licenses and the use of spectrum.

Why did the government do this?

If it didn’t save Vi, the government’s debt would never have been paid. Also, not saving Vi would leave only two private telecom companies, Bharti Airtel and Reliance Jio. That would create a duopoly, something which the government wants to avoid as competition is better for consumers.

Lastly, a conversion was chosen because the route of turning a company’s debt into its equity is less politically risky than an all-out cash bailout. The taxpayer needing to pay the losses of a private player doesn’t look good.

Problems Solved

With the government stepping in, Vodafone Idea finally gets the breathing room it desperately needed, both financially and strategically.

Reduced Interest Payment

The debt reduction from ₹2.2 lakh crore to ₹1.8 lakh crore means Vi's annual debt payments reduce from ₹40,000 Cr to around ₹18,000 - 23,000 Cr.

This extra breathing room allows Vi to refocus on business expansion. It is supported by a ₹55,000 Cr capex plan over the next three years, which requires careful execution.

Improved Investor Confidence

Vodafone Idea (Vi) needs funds to upgrade its technology. It can either raise more debt or more equity.

But, seeing it already has high debt, few lenders want to loan it more money. Vi’s credit rating for short-term debt is CARE A4+, and for long-term debt is CARE BB+. This means there is a high default risk.

The way out is to issue more shares to equity investors who enjoy higher risk. Even with government involvement, Vi is still risky, but having its liability reduced by ₹37,000 Cr makes it slightly less risky.

This is because thousands of crores are now free to be invested into productive assets that could stabilize Vi’s future. Now, investors who found Vi too risky before could be more comfortable investing in it.

Funding from these new investors is estimated at ₹25,000 Cr.

Government interference isn’t an issue either, as it decided not to take any board seats or management control. It wants Vi to remain private.

Problems Remaining

Money won’t buy happiness for Vi either. Although it now has more time, problems go deep.

Long-term financial viability

Vi’s underlying business fundamentals remain weak. The company had a net loss of ₹31,238 crore in FY24. Usually, sales growth is required to offset temporary losses in the promise of future profits. The company lost 17 Lakh+ wireless subscribers in 2024.

In telecom, the customer is highly price-sensitive. A solution to this is to invest in better technologies like 5G and offer them at higher prices.

But Vi barely has a 5G network & plans to invest in upgrading its 4G network at the same time as 5G. By still focusing on 4G, Vi is diverting funds from future technologies that could help it increase income.

Structural Debt Issues

Vi’s Debt/ EBITDA ratio was 14.8x before the dilution, while its competitors are around 2.5x. A lower ratio shows a company’s ability to clear its debt.

Even after the 17% reduction in AGR dues, Vi would take 10+ years before it could pay off its debt. A luxury it doesn’t have, seeing that 2031 is the deadline set by the Supreme Court.

To pay off debt, Vi must increase its ARPU, or average revenue per user. Currently, ARPU stands at ₹175 to Jio’s ₹205 & Airtel’s ₹240.

For Vi to be financially viable, it needs an ARPU of ₹300-380, which is higher than both its competitors. The funds needed to invest in CAPEX of ₹55,000 to increase ARPU also remain unclear.

The math doesn’t lie: Vi needs more users, a higher ARPU, and ₹55,000 Cr in capex it doesn’t yet have. Without real business revival, this may just be a pause, not a rescue.

MEME OF THE WEEK:

Dalal Street Dictionary

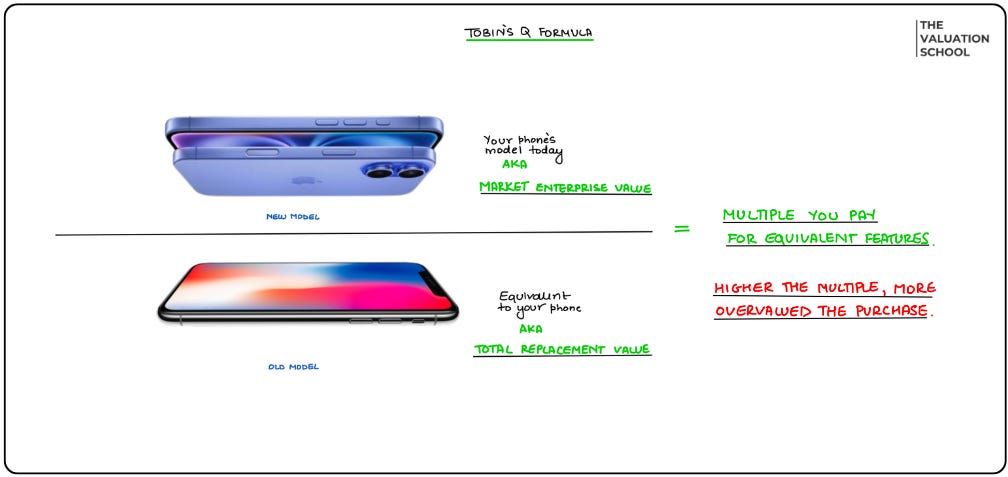

Why do people camp outside Apple stores for the latest iPhone when last year’s model works just fine?

The newest iPhone looks better and runs faster, but is it worth the premium over last year’s model?

Investors face a similar dilemma when valuing companies. Tobin’s Q helps them decide whether a company’s market price reflects its true worth, just like comparing the cost of the newest iPhone to the old one.

To calculate Tobin’s Q, we need two components:

For the numerator, the enterprise value (EV) is needed.

Enterprise Value = Market Capitalisation + Market Value of Debt - CashThis gives us the estimated price we’d need to pay for the company’s operating assets at market price.

For the denominator, we need the replacement cost of the company's assets. It is the cost to replace all the company's existing assets in their present condition at current prices.

If this ratio is equal to 1, we say the market is fairly valued. For example, if the cost to replace your iPhone is ₹50,000 and a new one with almost the same features is ₹150,000, Tobin’s Q is 3. The iPhone is overpriced.

But, how is it useful in markets?

Tobin’s Q is useful in understanding future supply in a sector. If Tobin’s Q is 2x, this tells us that for every ₹1 worth of assets, investors are paying ₹2. The sector might be overvalued.

This outsized reward for a lesser investment is attractive to new competitors to enter the industry. As a result, supply would increase, and prices of goods & services sold would decrease. Old investors would pay less to buy assets in this sector’s future opportunities due to high competition. Tobin’s Q would then return to 1.

This ability of the ratio to help see future sectors makes it important for making informed investment decisions.

What More Caught My Eye?

Almost ₹1,000 Cr penalty on Indigo!

Government eyes BHEL’s thermal power.

Second big win for Wipro in a year.

How is Pidilite diversifying away from Fevicol?

FM Nirmala Sitharaman: Reduced import duty for Trump’s America.

Recommendations

This week, I recommend watching an interview with the legendary Naval Ravikant. He is an entrepreneur, investor, and co-founder of AngelList. In this discussion with Chris Williamson, together they explore the timeless question of what it means to truly live well.

Thanks for reading this weekend’s newsletter. I’d like to know your thoughts, so please feel free to comment below. Your feedback helps us improve!

And don’t forget to like, share, and restack!

Song of the Week:

This is Parth Verma,

Signing off.

Sir I am a huge fan of you. Please sir can you make a separate video on Tobin's Q with real life examples of paint and cable industry where new companies are entering pushing the TOBIN'S Q towards 1

What a song 🫡