How to Analyse the Hotel Industry?

Our aim through TVS Weekly is to break down financial stories and concepts simply, explaining what happened and why it matters to you.

No Jargon, no drama! just stuff that actually makes sense.

Curious? Get more from us on our Instagram, WhatsApp, LinkedIn or YouTube. Our 800K+ family awaits you!

In this week’s newsletter, we’ll understand India's Hospitality Sector. We will learn:

Demand & Supply forces shaping the industry

Risks involved in the industry

How hotel chains manage to increase supply while managing risks smartly.

The Indian hotel industry is experiencing major growth because more people want rooms than hotels can provide. This gap between high demand growth and limited supply growth creates perfect conditions for hotels to succeed in the coming years.

So what exactly does this mean for travelers, investors, and the future of tourism in India?

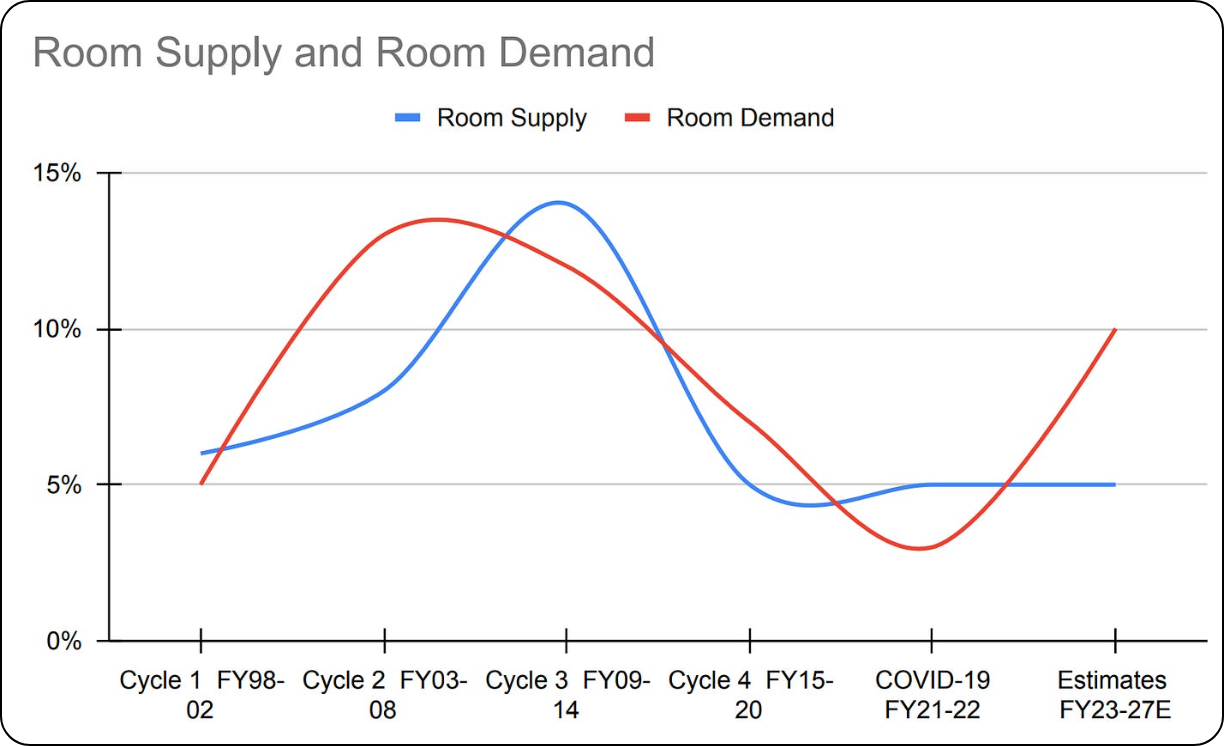

Demand & Supply

In the present scenario, supply and demand forces seem favourable towards an upcycle in the industry. For FY24- 27, supply is growing at the pace of 9% a year, while demand is growing at 12%. Let’s understand further.

Hotels Supply

To study the supply for hotels, we must understand:

Supply always lags behind hotels, and increasing it takes a long time.

The current stock of hotels.

Effect of the growing middle class on demand.

Supply Time Mismatch

Supply for rooms lags behind demand because it can't be increased quickly. A new hotel typically takes 4 to 6 years for construction and opening. Then it may need another 5 to 10 years to become profitable due to the high upfront investments required.

Supply comes from either building new properties (greenfield projects) or upgrading existing ones (brownfield projects).

Brownfield investments usually take less time to complete, but hotel operators often prefer greenfield projects when expanding into new, lesser-known, or unexpected destinations. In recent history, on average, greenfield investments have had the highest supply.

Supply stock for hotels

India has about 3.2 million hotel rooms, with only 0.2 million (6.25%) from branded hotels. This is far below China's 25% and the USA's 70%. Even within the branded hotel segment, the top 10 players operated around 1,500 hotels.

The industry is very fragmented with high competition. Customers have a lot of options. That being said, India’s share of hotel rooms per person is among the lowest globally. There is only 1 hotel room per 10,000 people in the country.

Rich & middle class influence

Investments are based on hotel segments.

Luxury (5-star)

Upper Upscale (4-5 star)

Upscale (3-4 star)

Mid-scale (3-star)

Economy (2-star).

Out of these segments, the current supply growth is maximum in the mid-scale and economy segments in tier-2 & 3 cities. These segments cater the most to the rising middle class as they earn more and spend on domestic tourism. This trend is expected to extend beyond FY27 till FY29.

Investments in Luxury properties have been the most stable while being less cyclical. The growth of this segment has been consistent at an average of 6-8% for the last 20 years. A likely reason for this is that luxury properties take the highest amount of time and investment. This ensures a limited supply.

Hotels Demand

To study the demand for hotels, we must understand:

Demand is cyclical & seasonal.

Domestic tourism as India grows rich.

Rise of religious & spiritual tourism.

Demand is cyclical & seasonal

Most hotel demand in India comes from domestic leisure spending on vacations, weekend trips, and get-togethers, which relies on consumers' discretionary income.

When the economy slows down, this optional spending on hotels is usually the first to decrease. This economic cycle takes years to complete and creates long-term demand patterns for hotels. Seasonality is a short-term version of this.

In seasonality, demand for hotels goes up and down based on events, desirable weather or festivals. Here are a few examples:

Wedding season (November-February and May-June, etc)

Holidays for festivals

Summer school vacations (May-June)

The times when such occasions don’t happen are considered the off-season for hotels. During off-seasons, guests are more price sensitive as they aren’t compelled to spend more to get a reservation on a particular time and date.

Domestic tourism as India grows rich

Demand for hotels is mainly split between demand for leisure and business. The individuals and companies that book hotels are increasingly becoming richer.

Let’s take the example of individuals & families. The current percentage of middle-class families is at 21% and is forecasted to reach 46% by FY2030. This growing wealth and later urbanisation are fueling demand for upscale and mid-scale hotel segments.

The rich have been increasing their spending, too. Luxury home sales have grown 7x in the last 5 years, with every foreign luxury brand enjoying consistent double-digit growth.

Business travel and M.I.C.E. (Meetings, Incentives, Conferences, and Exhibitions) tourism is expected to grow. Company earnings in the NIFTY are forecasted to grow at an average of 14% in FY24-27E, which is higher than nominal GDP estimates. High profits allow increased spending on travel.

Rise of religious & spiritual tourism

Revered destinations like Amritsar, Varanasi, Rishikesh, Kedarnath and Tirupati, among others are cultural hotspots. The demand for these destinations goes beyond generations.

For example, according to the Ministry of Tourism, significant spiritual hubs had approximately 1.43 billion visitors in 2022! These visitors need a place to stay.

But what risks might threaten this golden opportunity?

Risks involved in the industry

As per our understanding, there are two primary risk factors in hotels:

High upfront investment with delayed profitability

Fixed expenses with variable income

High upfront investment with delayed profitability

Hotels are very expensive to build, both in terms of cost and time. This is core to the business. On this, another layer of complexity is that until profitability is reached, the future performance of the hotel is unknown. Let’s take the example of 2008.

Here, due to the growth in demand outdoing supply growth, hotel operators invested aggressively. This increased supply dramatically reduced the ADR until 2022. Only after a more conservative supply growth in the last 10 years has the growth in demand gone ahead of supply. The effect of this is having higher ADRs.

For ten years, new hotels made less money as there were not enough guests for the supply built. This cyclicality makes it hard to predict when hotels will start making money, and even after they do, their profits stay unpredictable.

Fixed expenses with variable income

A good way to think of a hotel is in two major categories. First being the hotel itself with the second being the experience of the hotel. The first category depends on the location, design and maintenance of the property itself.

The second category depends on the quality of staff, service and food & beverages, among others. Notice that most of these costs are fixed in nature. The property needs to be maintained, the staff need a salary, and the electricity needs to be paid for

On the other hand, the hotel’s income is variable as it depends on guests coming in. The major sources of earnings are through room revenue (60% of revenue), food and beverage (33% of revenue) and other revenue (7% of revenue).

This timing mismatch makes managing cash flow difficult for hotels, especially during off-seasons when demand is low for months. Therefore, hotels are said to have a high operating leverage.

Before we understand how hotels manage risks, let's first learn their language.

Key Terms

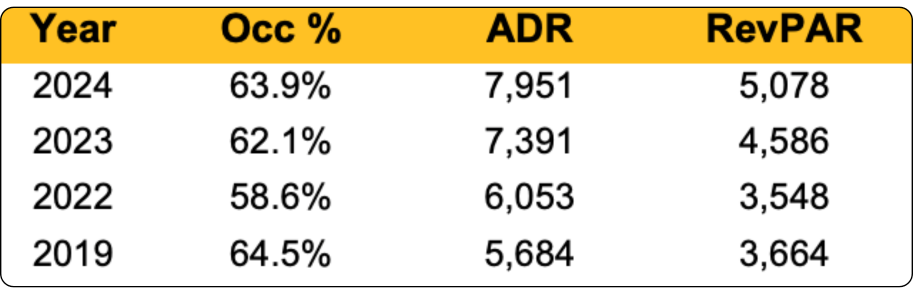

Average Daily Rate (ADR): The average price paid for rooms sold during a specific period. It is calculated by dividing total room revenue by the number of rooms sold, excluding unoccupied rooms. It is also known as Average Room Rate (ARR).

Revenue per Available Room (RevPAR): Similar to ADR, it is the average revenue earned by considering all rooms. It is calculated by dividing total room revenue by the total available rooms in the hotel, including the vacant ones.

Occupancy: The percentage of available rooms that are occupied during a specific time. It is calculated by dividing the number of rooms sold by the total available rooms.

Degree of Operating Leverage (DOL): A hotel's operating profit is highly sensitive to changes in revenue, measured by dividing the change in operating profit by the change in sales. This sensitivity (high DOL) means that when revenue drops, profits fall even faster. Hotels typically experience this effect because of their substantial fixed costs that must be paid regardless of earnings.

Keeping in mind these terms, hotel operators use scale and network effects to smartly deal with them.

How Hotel Chains Increase Supply & Manage Risk

Being a part of a chain has its advantages. Guests learn to trust the brand because they get similar experiences at different locations. But, mainly, hotel chains manage risk by:

Diversifying based on property & amenities.

Regularising Income.

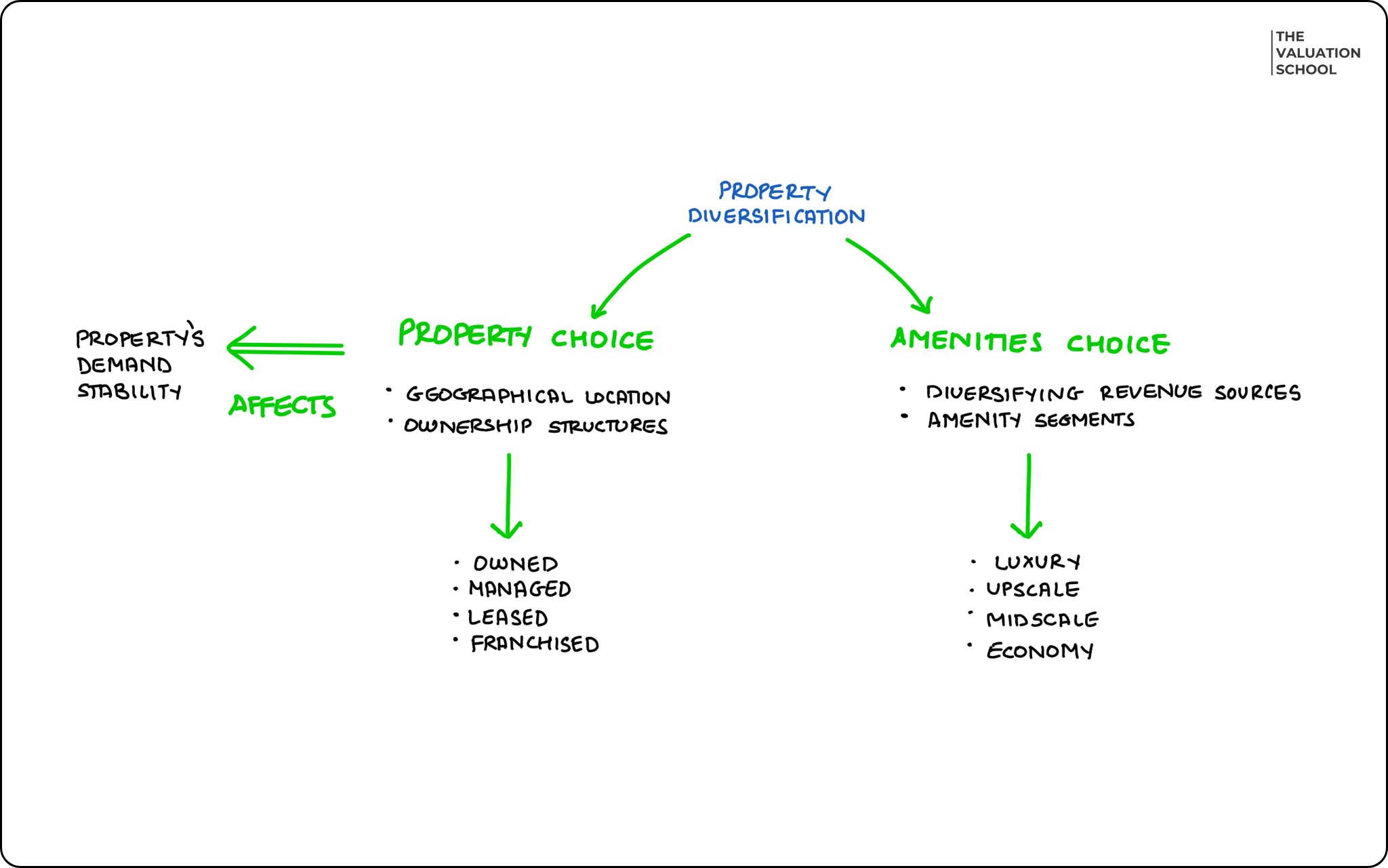

Diversifying based on property & amenities

Property Diversification can be done through having different property types and different amenities inside each property.

The end goal for any property is to reach relative demand stability regardless of season. This means having year-round occupancy of loyal guests or securing a strong location advantage.

Property Choice

Property choice mainly consists of a choice based on location and operations. Hotels in city centers, suburbs, or tourist spots get different numbers of guests. Hotel chains balance this out by having locations in various places, so when one spot is quiet, another can be busy.

Properties differ in their ownership as well. Properties can have different owners or operators. Let’s see a few:

Owned Hotels: The hotel company owns both the building and business operations. This gives them complete control over quality and decisions, but requires huge investments. They keep all profits but face all risks too.

Managed Hotels: Someone owns the building while a hotel brand manages daily operations. The owner provides the property and capital, while the brand contributes expertise and reputation.

Leased Hotels: The hotel brand pays rent to use someone else's property. This provides guaranteed income for the property owner and operational freedom for the brand. The brand takes more risk but keeps profits above the rent.

Franchised Hotels: The property owner runs the hotel independently but pays fees to use a recognised brand name. This allows brands to expand quickly with minimal investment.

Amenities Diversification

Amenities are desirable and useful features or facilities within the hotel. Offering better amenities helps to diversify revenue sources. For example, a better restaurant experience creates possibilities for guests to come to the restaurant even if they don’t stay.

The amenities provided by hotel chains depend on the segment in which the hotel exists. The more expensive the hotel, the more amenities. This is how hotels are segmented.

Each segment has different diversification opportunities. The segment and its set-up costs are:

Luxury Hotels (2.4 Cr per room): The benefit of having high-end properties is that demand for them is more stable compared to any other segment. Their success is highly dependent on location iconicness. They also have the highest ADR, RevPAR and contribution of food and beverage to revenue.

Upscale Hotels (1.7-1.1 Cr per room): Upscale hotels have the second highest occupancy levels of all segments. Business travellers prefer upscale hotels over luxury hotels. They are positioned to capture a lot of the rising demand for business travel.

Midscale Hotels (0.6 Cr per room): They can be thought of as midscale and upper-midscale. The upper-midscale category is dominated by foreign hotel operators, with the lower-midscale being with domestic players. Foreign players are keen to fulfill this demand as they get access to the Indian market with less investment and fewer staff.

Economy Hotels (0.4 Cr per room): Economy hotels are the most labour-intensive but with lower average investment. Their demand has mostly grown by domestic tourism. They are better positioned to capture demand in religious and spiritual tourism by the middle class.

Regularising Income

Hotel chains carefully balance ADR and RevPAR to manage cash flow. This is important as fixed costs need to be paid regardless of income. To earn stable cash, hotels tie up with companies, airlines to offer rooms to their employees at a lower rate.

Loyalty programs that offer rooms at lower rates to members are another way to help demand during off-seasons. Due to offering rooms at a lower price, the average revenue falls.

But, since occupancy is up the revenue considering all rooms or RevPAR increases as total revenue is higher. A more stable source of income would also lead to a lower operating leverage.

India's hotel chains appear to have learned valuable lessons from the 2005-2008 overexpansion, now carefully matching supply growth to stay below demand forecasts through 2027. It remains to be seen if this measured approach delivers the sustainable profitability the industry has been waiting for.

And with that, we wrap up this month’s sector deep dive! I’d love to know your thoughts about our discussion, so feel free to comment below.

And don’t forget to like, share, and restack

Song of the Week:

This is Parth Verma,

Signing off.

Insightful. A request to please do a detailed piece on the power and energy industries.

I'm an Hotel Management grad from IHM Mumbai, who's very much into finance. Loved your analysis.