Rethinking the Hospital Sector: A Guide

Our aim through TVS Weekly is to break down financial stories and concepts simply, explaining what happened and why it matters to you.

No Jargon, no drama! Just stuff that actually makes sense.

Curious? Get more from us on our Instagram, WhatsApp, LinkedIn or YouTube. Our 960k+ family awaits you!

In this week’s newsletter, we will be learning:

The demand & supply characteristics of hospitals.

Key risks faced by hospitals.

Evolving Strategies used to manage risks in increasing supply

What kind of business turns away demand, not because it can’t serve more, but because growing too fast might kill margins?

Welcome to the hospital industry. A sector where competition is brutal, demand is uneven, and expansion is a strategic chessboard.

Despite being flooded with patients, top hospital chains grow carefully by using their profits. They often double down in the cities they already operate in rather than spreading thin.

Why? Because this game isn’t just about beds and machines. It’s about control, capital, and consistency.

In this deep dive, we unpack how hospitals are expanding with surgical precision and why demand shows up where it does.

Demand for Hospitals

To understand demand for hospitals, you must understand:

Stratified Demand Sources

Structural Demand Difference

Insurance & Demand

Stratified Demand Sources

The healthcare sector is hospital-centric, with its contribution to 80% of the healthcare spending, most of which comes from private hospitals. They account for 55% of the total.

One demands for hospitals based on their needs, and with each patient having different needs, the way people demand hospital services is diverse. They are thought of as:

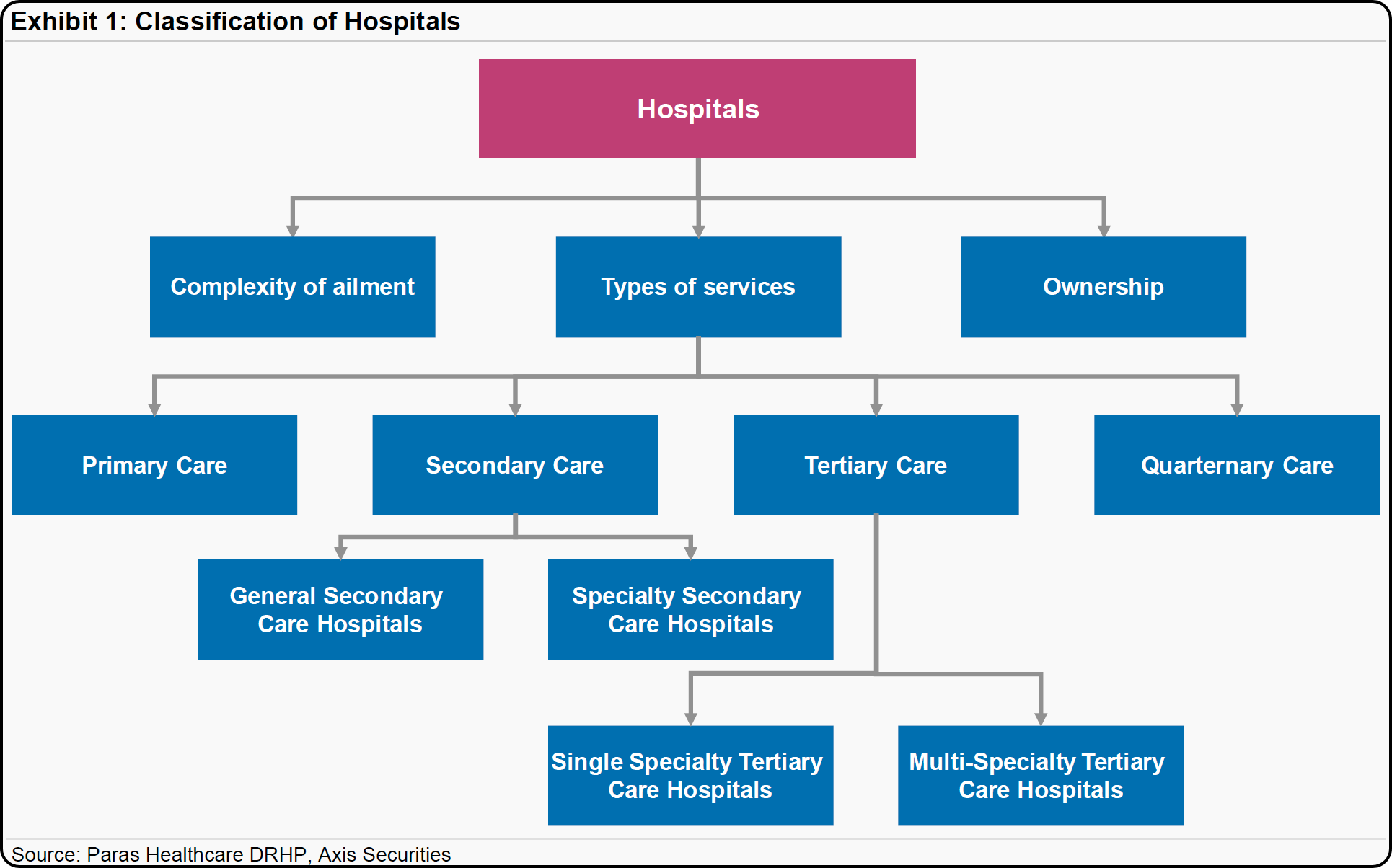

Level of care-based demand

Primary, secondary, tertiary and quaternary care refer to the complexity and severity of health challenges that are addressed, as well as the nature of the patient-provider relationship.

Primary care is the first point of contact, focusing on prevention and treating minor illnesses, similar to a family doctor. With no inpatient beds, demand comes from outpatient visits, and investment is low.

Secondary care offers specialised services after a referral, handling complex conditions like cardiology treatments. With 50-200 beds, it serves inpatient and outpatient needs, requiring moderate investment.

Tertiary care provides advanced treatments for severe conditions, like cancer, in hospitals with 200+ beds. Demand is mostly inpatient, with significant investments.

Quaternary care offers rare, experimental treatments in specialised centres. Due to its exclusivity and complexity, it requires the highest investment.

Structural Demand Difference

Compared to the global standard, the number of beds in India is only 1.3 beds per 1,000 people, where the global average is around 3 beds per person. There is huge headroom for growth for consistent revenue.

Consistent because demand persists even in down cycles as people still get sick & require operations.

Demand is also uneven and concentrated. Delhi can serve patients up to Rajasthan and beyond, as demand for many places flows to only medical hubs, making the demand uneven.

Insurance & Demand

The insurance sector serves as a demand booster for the hospital industry. This is because paying for treatments & surgeries out of pocket is too expensive for most Indians.

This limits the number of people hospitals can reach.

This is where the phenomenal growth in the insurance sector has helped hospitals help more patients, as it continues to grow at an annual rate of 18% and is expected to extend coverage to 33 Lakh more individuals till FY27.

Supply of Hospitals

Constraints to increasing supply

Historical Capex Characteristics

Constraints to Increasing Supply

The immense demand for hospitals is seen by each hospital player as headroom to increase their supply. But constraints exist, and they differ for each player based on their size.

At the smaller sizes, there are numerous small doctor-owned clinics. These form a major part of the industry. Competition is the highest here.

When we get to the hospital level, 80% of them stand alone, with high fragmentation being experienced here too.

However, when it comes to large super-speciality hospitals, they face very different levels of competitive intensity.

Their large size works in their favour, as high investment needs create a barrier to entry. New hospitals lose money at first and must build scale, reputation, and specialisation over time.

Even within big hospitals, specialisation matters. Seeing the cost structure, hospitals get more expensive the more specialised they become, as it means a higher proportion of equipment cost as a percentage of total cost.

Historical Capex Characteristics

We’ve established so far that hospitals are expensive to build, maintain & routinely upgrade.

To get this done, hospitals could reach into their CFOs (cash flow from operations), but for larger investments like building new hospitals where the payoff could take years, they relied on debt.

As hospital chains kept on engaging in capex, they kept taking on more and more debt to finance it.

Risks in the Hospital Industry

To understand the risks involved in the hospital industry, we must understand:

Oversupply risk in key locations.

Price Taking & Hurdles in Establishing Presence.

Cash Flow Challenges from Slow Payors

Oversupply risk in key locations.

Supply is concentrated in a few cities, with up to 80% of revenue for key players like Max Healthcare coming from Delhi NCR. This makes hospitals vulnerable to economic or regulatory changes in these regions.

Further, the rate of expansion matters too.

For example, in 2016, the ₹4,100 crore in capex to increase the number of beds resulted in a temporary oversupply. Even though demand is high, the absorption rate for new capacity is slow.

This means that hospitals have ample room to increase supply, but they must be careful with the rate of increase.

Beds for complex surgeries take time to fill, and super-specialist doctors are scarce, which slows down how quickly new capacity gets fully used.

To maintain occupancy, hospitals shifted to government-backed patients and less complex surgeries, resulting in lower margins.

Price Taking & Hurdles in Establishing Presence.

Some hospitals perform better based on their size and age, known as "presence."

Large hospitals can offer more specialised & hence more expensive treatments.

Also, they have other add-on healthcare services like diagnostics & pharmacy in the same hospital, offering these services alongside highly specialised treatments increases their revenue per patient.

Older hospitals benefit from having already recovered construction costs.

Building this presence takes time and investment, but patient choice and government regulations add challenges. In a competitive industry, where healthcare is costly, many patients choose hospitals based on price.

Hospitals often become price takers for many procedures.

Government regulations fix procedure prices and cap costs for treatments and medicines.

For example, the government caps Cobalt Chromium Knee Implants at ₹55,000, about a third of their original price.

Cash Flow Challenges from Slow Payors

In healthcare, a payor is an entity that pays for the services provided by healthcare providers. These can be public or private insurance, government schemes, non-profits, or self-pay cash payments.

Payors differ in the amount they pay and the speed of payment. Insurance companies pay a pre-negotiated amount, while government schemes often delay payments.

Hospitals relying heavily on government payments face challenges in managing cash flow and reinvesting, as they don’t have cash on hand. Government hospitals are especially affected.

This issue arises because hospitals have fixed payments for staff, utilities, property interest, equipment, and suppliers. A slow payor mix can cause cash flow problems.

To truly understand these risks and how hospitals navigate them, it helps to know a few key terms used in the industry.

Key Terms:

Bed occupancy: The percentage of available beds that are occupied by patients, indicating hospital utilisation. The higher the better.

Average revenue per occupied bed (ARPOB): The total revenue earned per day from occupied beds, divided by the number of inpatients.

Average length of stay (ALOS): The average number of days a patient stays in the hospital, calculated as total bed days divided by the number of patients. Different ailments have different ALOS. The lower the better.

Mix of treatments/ specialities: The variety of medical treatments offered, with more expensive treatments (e.g., transplants) increasing revenue.

Payor Mix: The distribution of patients based on the type of payor (e.g., insurance, government schemes, private payments), which impacts revenue collection and cash flow timings.

Investment per bed: The amount of capital invested in each bed, including infrastructure, equipment, and facilities.

How Hospitals Are Evolving with Surgical Precision

To understand how hospitals are evolving to meet demand, we must understand:

Brownfield Investments to further their presence.

Greenfielding safely.

Improving Speciality Mix.

Attending their Payor Mix

Taking Advantage of Medical Tourism Tailwinds

Brownfield Investments to further its presence.

Hospitals gain more by doubling down on their existing infrastructure in high-demand areas than by creating new ones in newer areas.

There are two reasons for this.

Firstly, hospitals don’t have to suffer lower occupancy rates or take on lower-quality patients to fill beds.

Secondly, reinvesting in existing properties directly boosts ABROB (Average Revenue per Occupied Bed). This is done by using the investment to add more specialised services and ancillary services like diagnostics or pharmacies.

It also includes increasing the number of beds to support these new offerings.

For example, Max Healthcare, a market leader in the Delhi-NCR and Mumbai regions, plans to add 3,000 beds over the next three years, primarily through brownfield expansions.

Greenfielding Safely

Another way to expand presence is by adopting different business models. Currently, hospitals use:

Lease Contracts: Leasing space in high-demand areas helps hospitals avoid ownership costs.

Operations & Maintenance (O&M) Contracts: Managing third-party healthcare facilities generates steady income and expands reach.

Franchise Agreements: Partnering with local operators helps grow the brand with minimal investment.

The O&M and lease contracts business model can be used to reduce initial investment for hospitals to lower their risk. Hospitals typically use asset-light models in two cases:

Big cities, where owning land is expensive.

Tier 2 & lower cities, where they lack an existing presence.

For example, Max Healthcare used an O&M agreement in 2022 for the first asset-light model in Dwarka, Delhi, with over 300 beds.

The "asset-light" model provides an appealing return on capital employed (ROCE) with minimal development risk, as the investment is limited to approximately 30-35% of the project costs.

For this strategy, hospitals work with real estate developers who can build the hospital facilities as per their specifications. Hospitals then manage them, leveraging their brand and expertise.

Improving Speciality Mix

Improving a hospital's speciality mix involves three key factors. Availability of specialist doctors, specialised equipment, and a focus on high-benefit specialities.

When talking about the highly specialised doctors & support staff themselves, they are a scarce resource. High attrition rates are also a problem.

To make specialists & other healthcare staff more available, hospitals can turn to internally generated training programs instead of all the pressure going to constant hiring.

Once doctors are more available, technology can enhance the highest-yielding specialities, boosting ARPOB and occupancy rates. Oncology and cardiology are leading the way in specialised care.

Oncology: With better access and early diagnosis, cancer care is advancing fast. It's now the fastest-growing speciality, with a 17% CAGR. Revenue has doubled from FY2020 to FY2024 in providing cancer care.

An example of recent investments in oncology tech enhancements is that the Fortis Memorial Research Institute recently introduced a ₹75 crore MRI-integrated LINAC machine, combining real-time MRI with radiation for more precise cancer treatment.

Cardiology: As more people seek timely treatment for heart-related issues, hospitals are stepping up their cardiac care offerings. The segment has grown at 12% CAGR since FY2020, with per patient revenue between ₹2–3 lakhs.

An example of recent investments in oncology tech enhancements is that Fortis Healthcare’s comprehensive care, including 12 Cath Labs and India’s first AICD implant, places it at the forefront of other competitors.

Attending to Payor Mix

A healthy payor improves patient inflow by making healthcare more accessible through insurance. Right now, insurance payments make up 36% of hospital revenue.

This share could grow to 50% soon. The reason? The insurance sector is expanding fast, at 30% per year. That’s a powerful growth driver.

Hospitals can improve their payor mix by reducing reliance on non-insurance or self-pay sources, like government schemes that delay payments.

Max Saket and Max Nanavati, for example, have strong, high-quality payor mixes.

Taking Advantage of Medical Tourism Tailwinds

Another focus can be capitalising on the growth of Medical Tourism. In the last decade, international patient inflow has surged from 1.8 Lakhs to 7 Lakhs, primarily for complex surgeries that yield high margins.

Specifically, private hospitals like Fortis, Max, Narayana, and Medanta have seen international patient revenue grow at 10% CAGR. They expect this to double in the coming years.

Foreign patients, who contributed just 3.5% in 2020, could account for 10–15% of revenue soon.

This is a win-win for both the hospital & patient. For hospitals, these patients often pay for these complex, high-margin surgeries in cash or through insurance. It’s a win for foreign patients as they enjoy significant savings.

For example, a heart bypass costs $5,200 in India versus $140,000 in the U.S.

In conclusion:

The hospital sector is expected to grow strongly under the weight of its own profits.

Health awareness is rising. Insurance coverage has increased, giving more people access to healthcare. Medical tourism is picking up. Further, hospitals are expanding capacity only when it can be absorbed.

Those who grow with the right mix of patients and specialities are best placed to succeed.

And with that, we wrap up this month’s sector deep dive! I’d love to know your thoughts about our discussion, so feel free to comment below.

And don’t forget to like, share, and restack

Song of the Week:

This is Parth Verma,

Signing off.

This was absolutely insane, mind blowing!!!!

For me Medical tourism is new topic to know more about as india is best place to visit and we deliver Better ayurveda treatment than anything else so may be there should some connection. I am excited to find this connection and thank you for this deep newsletter.