Ordering more Blinkit than Zomato?

Our aim through TVS Weekly is to break down financial stories and concepts simply, explaining what happened and why it matters to you.

No jargon, no drama, just stuff that actually makes sense!

Curious? Get more from us on our Instagram, WhatsApp, LinkedIn or YouTube. Our 1 Million+ family awaits you!

In this week’s newsletter, we will be learning:

How Blinkit is bigger than Zomato!

The importance of Sustainable Growth Rate.

My advice on staying organised during research!

Market Kya Keh Raha Hai, Sir?

Blinkit just flew ahead of Zomato in revenue this quarter.

₹2,400 crore vs ₹2,261 crore.

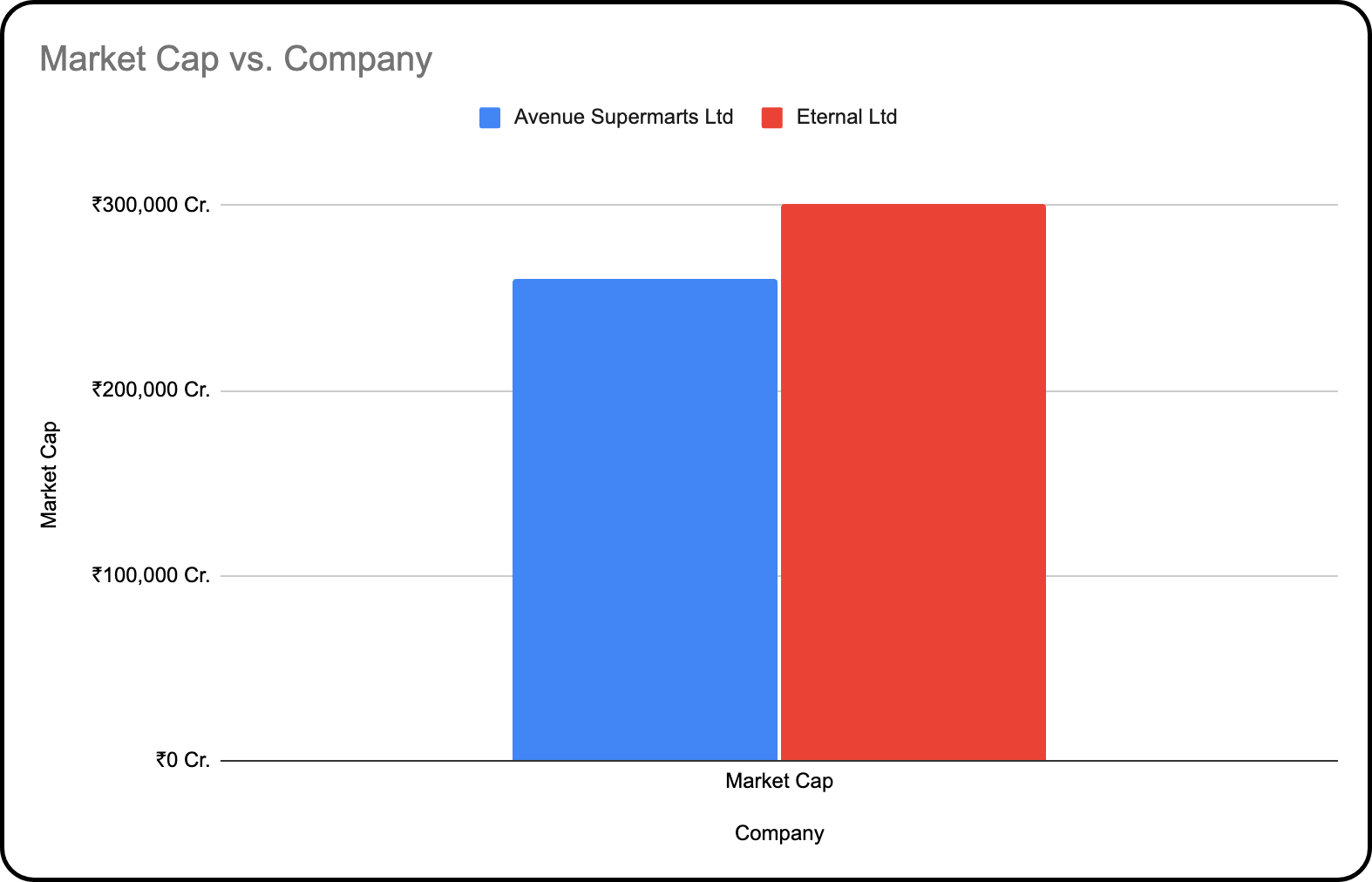

The stock jumped 15% as Eternal’s valuation went higher than DMart's.

But that’s just the headline.

The real story? India’s retail skipped a step. Quick commerce isn’t just growing fast; it’s reshaping how, what, and where we buy.

This week, we break down Blinkit’s breakout, the economics behind it, and what comes next as the category tries to be everything for everyone.

Blinkit is King

In its Q1 FY26 results, Eternal shared a key shift: Blinkit has overtaken Zomato in revenue, reaching ₹2,400 crore versus Zomato’s ₹2,261 crore.

Blinkit’s net order value jumped 127% as it has been able to scale fast while narrowing losses.

The management attributed this to Blinkit’s ability to focus solely on its customers’ need for value, and not price.

That focus paid off, as each new customer type Blinkit targeted covered fixed costs within the first month itself. This freed up cash to reinvest and grow faster.

But Blinkit’s story isn’t growing in isolation; it comes as a consequence of its industry.

The Rise of Quick Commerce

Quick commerce’s gross order value, which is the total value of items ordered before discounts or returns, grew 24 times in three years to reach $7.1 billion by FY25.

Monthly users doubled to 26.3 million. Those numbers have made it the fastest-growing Indian industry ever.

Blinkit, being the largest player in the industry, benefited.

Even considering this hypergrowth, quick commerce is expected to grow at a 40-60% CAGR till FY 2031!

Why did this happen?

The strange thing about quick commerce is that it’s a very Indian thing. The Indian retail environment contains parts that no Western country does.

High population density

Large, unorganised, and inefficient supply chain.

Low rider cost relative to the average order value.

India’s dense cities and messy retail make quick delivery more efficient than store visits. Low delivery costs help too.

The Problems with Leapfrogging

Developed countries moved in stages: kirana-style stores, then supermarkets, then quick commerce. India skipped the middle and jumped straight to quick commerce.

This has given rise to a few problems.

Traditional retailers suffer - Quick commerce pushes out local shops by using foreign money for discounts and private supply chains.

The middlemen get crushed - Most Blinkit riders earn ₹1.5 to ₹5 lakh a year, but with no job security or benefits. Their income depends on app targets, pushing them to rush, skip breaks, and risk their safety daily.

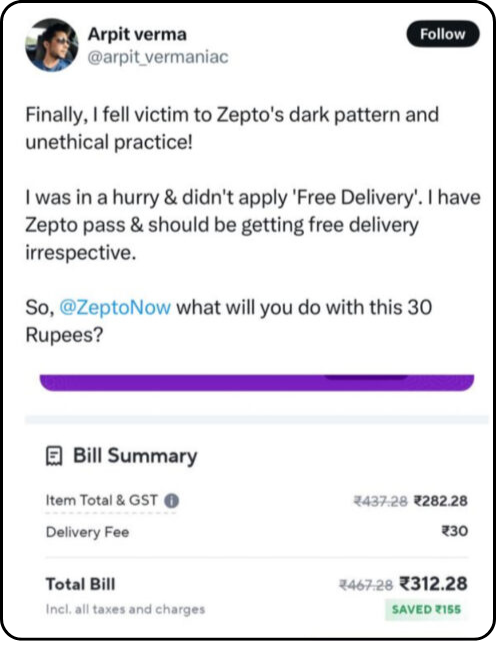

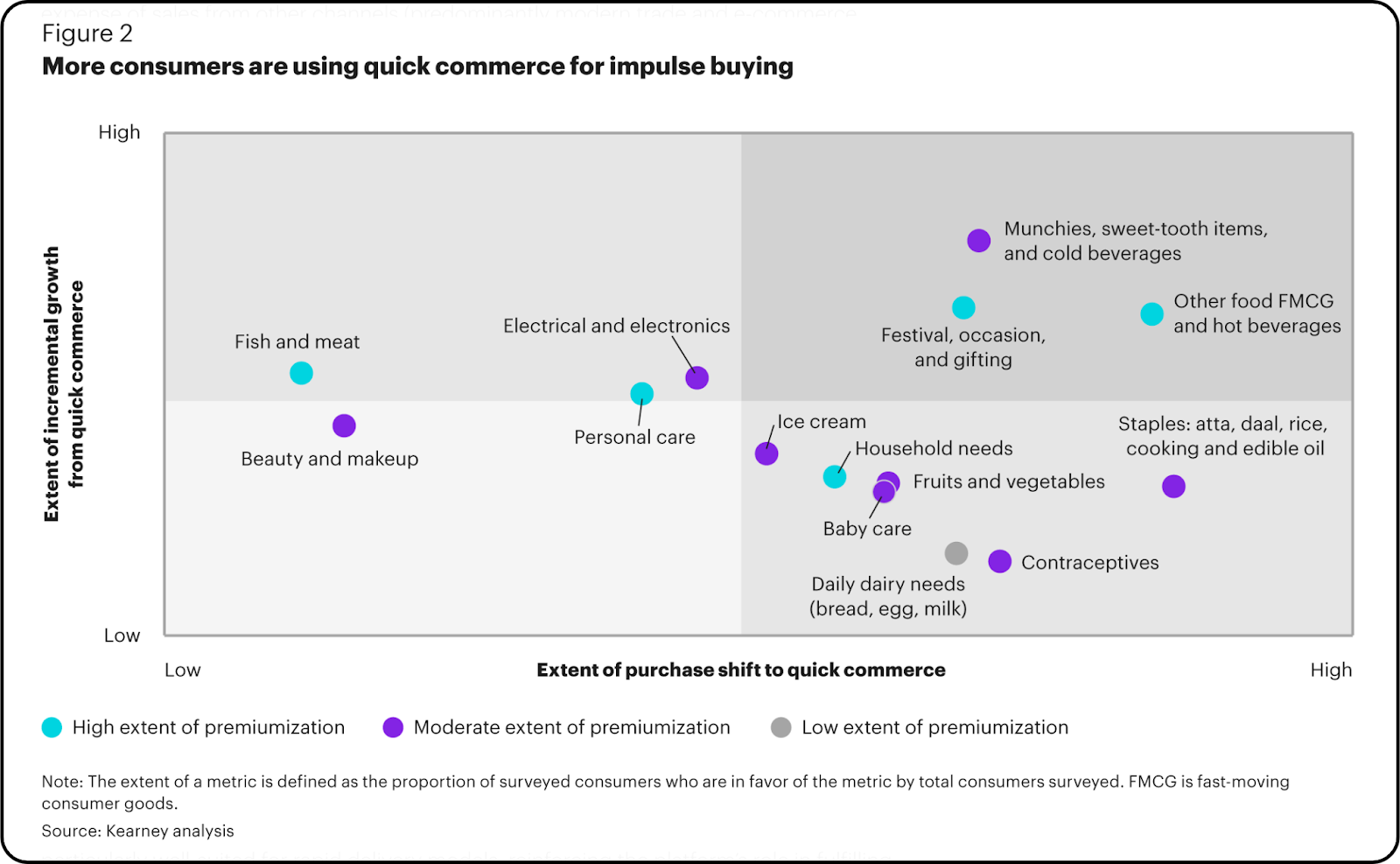

Convenience at a price - Quick commerce apps use hidden fees, fake urgency, and price changes to raise bills. They rely heavily on impulse purchases to drive revenue.

A Rush to be Everything to Everyone

As the industry grows and customers become used to the convenience, quick commerce isn’t stopping at groceries. There’s Snabbit for quick help or Slikk for beauty & fashion.

Existing platforms like Zepto, Blinkit & Instamart all have hot food offerings. Swiggy even went further this year by introducing Pyng, which helps hire professionals like therapists, CAs, and even astrologers!

That being said, all these players are relatively young when compared to their e-commerce peers like Amazon, Flipkart, or BigBasket.

Amazon & Flipkart entered late, but even with their strength, they lag in scale. BigBasket is struggling with a complex supply chain in its offered categories and poor UX.

Most of all, these players struggle to convince customers to pick them over the big three.

Nothing they cannot value

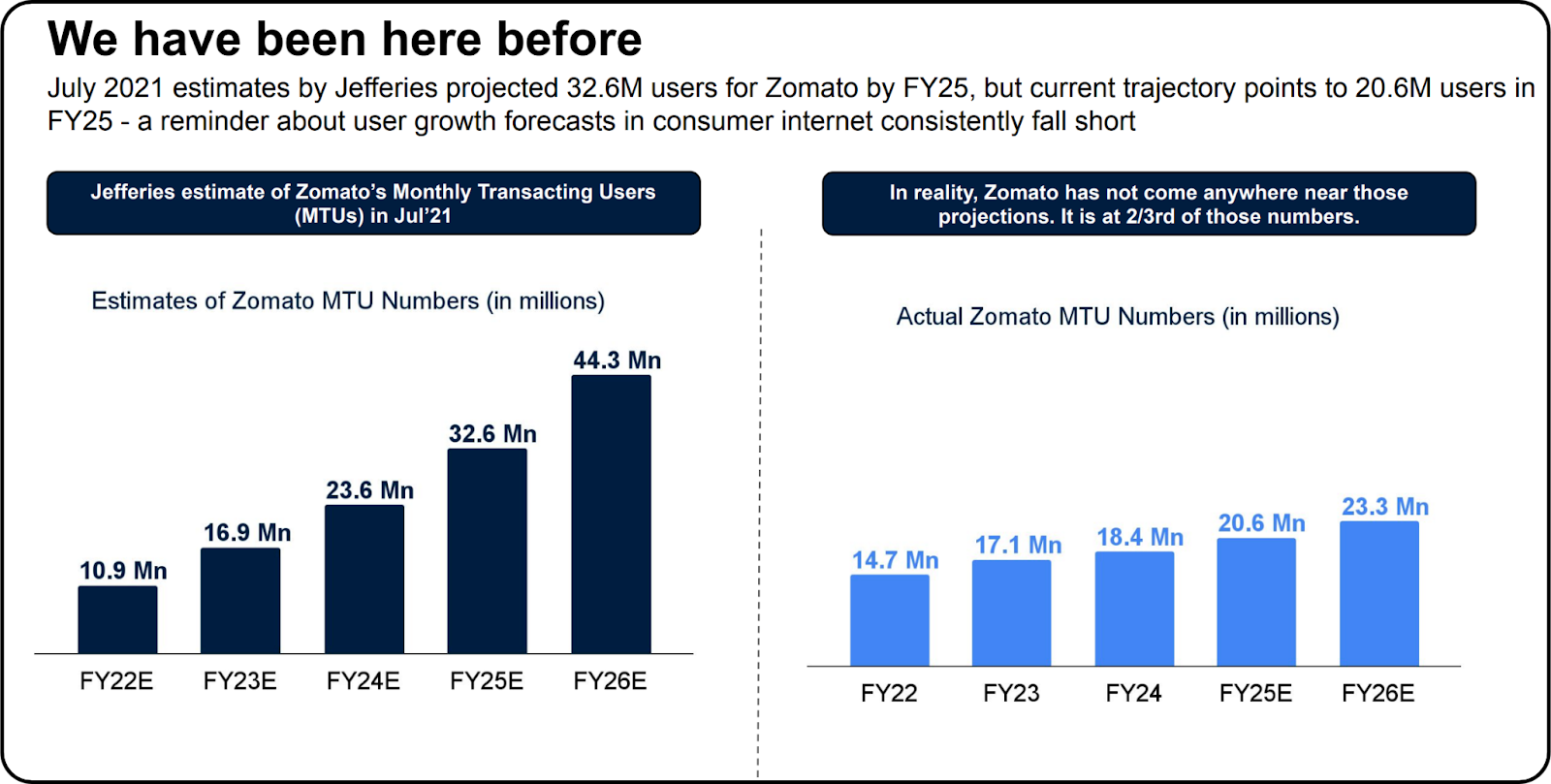

As quick commerce players struggle to capture a part of industry growth, similarly, investors and analysts struggle to put a price on that growth.

Why? Because future exponential growth is hard to value for both companies and analysts.

This is because companies often overestimate it, leading to financial strain.

Analysts, meanwhile, tend to use linear tools like valuation multiples that fail to capture nonlinear growth, causing mispricing and missed opportunities in high-growth businesses.

Further, quick commerce itself is a competitive industry whose target group of convenience-hungry users is small. The top 8–10M super consumers, which quick commerce targets, are growing slowly.

As growth slows, marginal users offer lower order value, raising doubts on scale and sustainability.

In conclusion, India skipped the retail middle step and went from kiranas to quick commerce. Blinkit’s surge proves the model can work and is paying off at present.

But scaling it nationwide won’t be so simple, as expectations & problems rise as the sector grows.

Until then, only time will tell.

So, is quick commerce worth the hype? Tell me in the comments!

Dalal Street Dictionary

Ever seen a momo stall grow from one tiny cart to a mini chain across your college area? Let’s say that stall makes ₹1,000 a day and reinvests ₹500 to buy better steamers or open a second spot.

That’s how fast it can grow on its own, without asking anyone for extra cash. That’s exactly what Sustainable Growth Rate (SGR) tells you.

It’s the natural speed limit at which a company can grow, powered only by its own profits.

SGR shows how much a firm can expand its sales and earnings every year without needing loans or new equity. It’s a smart way to check how self-reliant a business really is.

Here’s how you find it:

But, how is it useful in markets?

SGR tells us how healthy and self-reliant a company’s growth is.

Reveals growth stage: Is the firm still scaling fast, or has it hit maturity? SGR helps you judge that.

Guides financing choices: If a firm grows faster than SGR, it may need to raise funds. Slower than SGR? It still has a runway with its own profits.

Signals strategy fit: A high SGR firm likely reinvests more and prefers equity. Low SGR firms may favour safety, payouts, or slow-and-steady paths.

Kaam Ki Baat!

Disorganisation isn’t a focus problem.

It’s a system problem.

The real issue? You’re collecting, not processing.

Saving PDFs, bookmarking tabs, copying paragraphs, and calling it research.

But when you return, everything feels scattered.

Here’s a better way:

→ Create one master doc per company — that’s your central research note.

→ Break it into fixed sections: Governance, Business Model, Risks, Valuation, News Tracker or others.

→ Every update? Add the date + source + takeaway under the right section.

→ Keep a running track of what is changing.

Organising data while doing research isn’t only about being neat; it should also be retrievable.

So ask yourself:

If you had to use this research a month later, would you know where to look?

If not, it’s not organised.

Redesign your research habit because in equity research, speed matters, especially during the results season.

Struggling with your research flow?

Please comment below, and I’ll answer one each week.

MEME OF THE WEEK:

What Else Caught My Eye?

Biggest drop in share price recently!

India-UK finally sign FTA.

Where do companies go wrong?

End of the road for Good Glamm Group.

Why did Adani exit FMCG?

Recommendations

This week I recommend watching a special Moneytalks by Groww episode featuring Monika Halan. In under an hour, she shares sharp, practical advice on money, investing, and planning as a couple.

A must-watch for young professionals building their financial future.

Thanks for reading this weekend’s newsletter. I’d like to know your thoughts, so please feel free to comment below. Your feedback helps us improve!

And don’t forget to like, share, and restack!

Song of the Week:

This is Parth Verma,

Signing off.

Zomato's revenue lower than Blinkit but I feel Zomato still has not taped real growth, I believe it still has scope to improve. Middle class people still prefer to go to Kirana store and buy stuff mostly for entire month. They buy from quick commerce only in urgency or being lazy( telling from personal experience) I believe middle class people do check a lot while paying money on quick commerce if it is high eventually cancels transaction. And hidden fees are always there so if quick commerce wants to increase they should work on this otherwise normal people are not coming for them.

So first of all, as always, a great breakdown. Thanks for sharing this knowledgeable newsletter, Parth Sir and The Valuation School Team.

If we talk about e-commerce, the gap is still wide for Blinkit. Most of the revenue is generated from metropolitan cities like Delhi, Bangalore, etc. If Blinkit has to grow, it has to tap the untapped market, that is, Tier II, Tier III cities, or penetrate more into rural areas.

But if we also see the mindset of an Indian middle to lower-class consumer, whose daily needs are sometimes on a credit basis at most Kiryana stores, in my opinion, Quick Commerce is still overvalued.

Because at the end of the day, e-commerce companies have to penetrate themselves into more areas. Time will tell how Tier II and Tier III people will react to this change from Kiryana stores to Quick Commerce apps.